Cardinity is now part of

It's safe to say that almost everyone in the UK has used a Chip and PIN machine regularly. It’s potentially one of the most recognisable and trusted payment methods.

Chip and PIN is actually a brand name, officially known as EMV Cards or EMV Chip Cards because it was developed by Europay, Mastercard and Visa (EMV). It was introduced to create a global system for accepting credit and debit card payments that are more secure, faster and easier to use than previous methods. We can easily say they were successful in achieving this.

But while Chip and PIN remains an essential part of modern payments, the industry has continued to evolve rapidly. Contactless payments, digital wallets and local payment methods are now shaping the future of point-of-sale (POS) experiences.

Although you know what Chip and PIN is, do you really know how it works and all the different types available? Let’s get into it!

What’s in this blog:

Chip and PIN is a secure payment method used for face-to-face transactions, most commonly in shops and hospitality. It allows businesses to easily and quickly accept credit and debit card payments using a payment terminal or card machine.

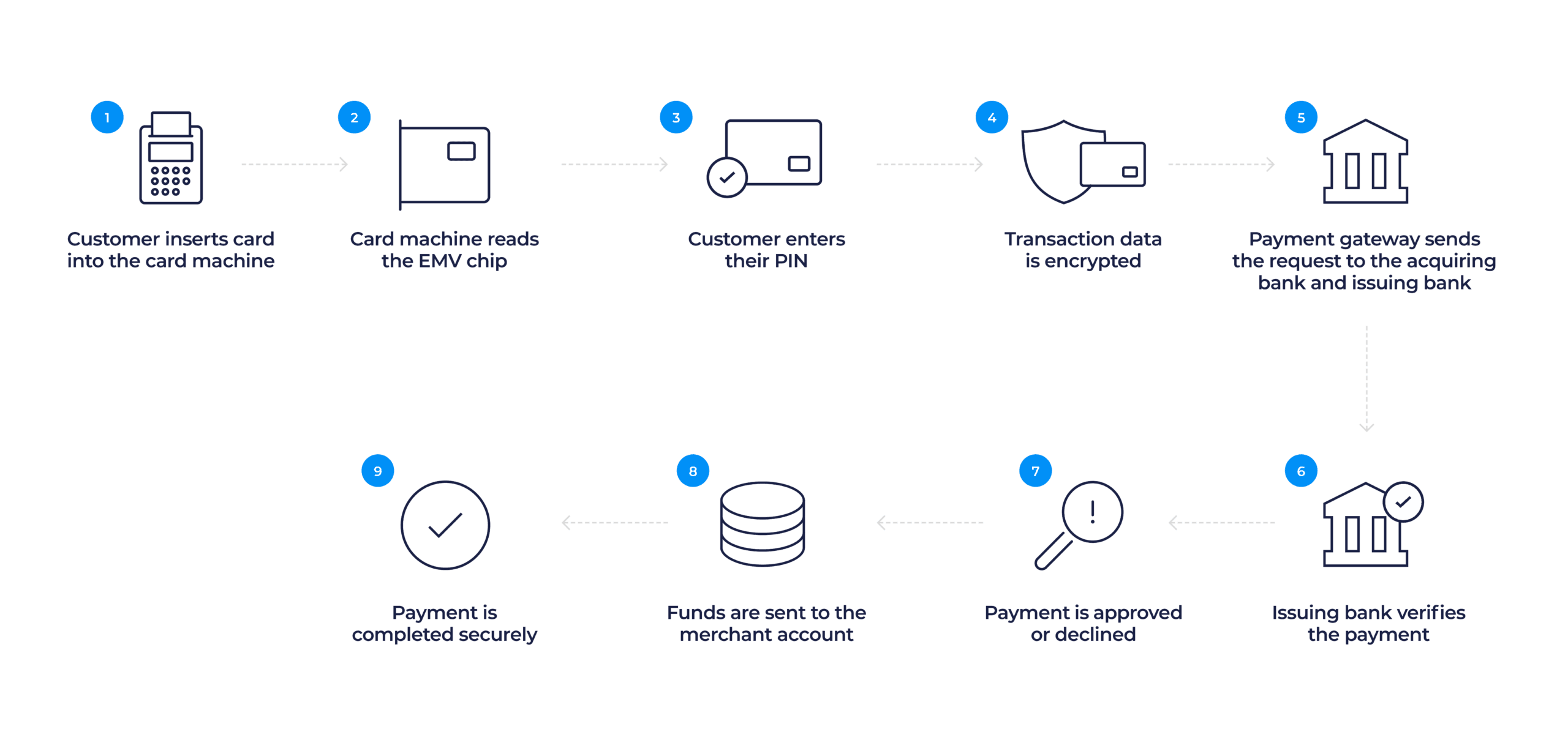

Unlike older magnetic stripe cards, Chip and PIN cards contain an embedded EMV microchip that securely stores encrypted payment information. During a transaction, the customer inserts their card into the card reader and enters their unique Personal Identification Number (PIN) to authorise the payment.

Chip and PIN technology is now used globally and, with the combination of chip authentication and PIN verification, it remains one of the most secure forms of card-present payment processing.

Modern POS systems and card readers also support contactless payments, digital wallets and mobile payment methods alongside traditional Chip and PIN transactions.

With Chip and PIN, cards contain an EMV microchip that securely stores payment information about the account holder, including their name, account number and card expiry date. The cardholder then has a unique 4-digit PIN.

When a customer is ready to pay, they insert their card into the machine and enter their PIN. The Chip and PIN machine then securely processes the payment by communicating encrypted transaction data between the payment gateway, acquiring bank and issuing bank. Once it has been authorised the amount will be transferred to your merchant account.

The best part about a Chip and PIN payment system is that it is all done automatically in just a few seconds, allowing businesses to take card payments quickly and securely.

Chip and PIN cards can also be used to withdraw money from an ATM in the same way.

Chip and PIN was introduced in the UK in 2004 but it became mandatory for all cards in 2006, replacing the older magnetic swipe method. Other countries also adopted EMV technology as part of a wider move towards more secure global payment standards.

The swipe method involved physically swiping a card and then comparing signatures. It was slow, lacked security measures and prone to fraud. So, Chip and PIN cards were introduced to combat these issues to enhance security and reduce card payment fraud.

In fact, during the first few years of Chip and PIN payments in the UK, there was a reduction in card payment fraud, with annual counterfeit card fraud losses down £81.9 million.

Today, EMV Chip and PIN technology is used worldwide to help reduce card fraud and improve payment security for both businesses and consumers.

There are a few types of card machines available to suit different business models and payment environments:

Countertop card machines: These are commonly found at the main point of sale or checkout in shops. They require a connection to the mains and your WiFi or phone line.

Portable card machines: These are popular in restaurants, bars or cafes. They allow you to take payments anywhere in your business and consist of a card reader and a base unit connected via Bluetooth or WiFi.

Mobile machines: These machines are ideal for businesses on the move. They use a built-in SIM card and mobile data connection, allowing you to take payments anywhere with a signal.

Smart POS systems: Modern POS systems can do much more than simply process Chip and PIN payments. Many now include:

Digital receipt functionalityBusinesses increasingly choose POS systems that support both traditional Chip and PIN payments and modern digital payment methods.

Why not check out the POS solutions we have available for your in-store checkout?

In addition to Chip and PIN, many cards now support contactless payments. Contactless payments involve tapping the card on a reader for payments up to £100. They have become increasingly popular due to their speed and convenience.

Card readers will accept both Chip and PIN and contactless payments, as well as digital wallets like Apple Pay and Google Pay. As cashless transactions continue to grow globally, the use of Chip and PIN and contactless payments will increase.

While Chip and PIN transformed card payment security, consumer payment preferences continue to evolve rapidly.

Today’s customers expect businesses to offer flexible payment experiences that go beyond traditional card payments. Alongside Chip and PIN and contactless transactions, many consumers now use:

Different countries and regions also have preferred local payment methods. For example:

As global commerce continues to grow, businesses increasingly need payment solutions and POS systems that can support both international card schemes and local payment preferences.

Offering the right mix of payment methods can improve customer experience, increase conversion rates and help businesses expand into new markets more easily.

Modern POS systems are designed to support far more than traditional Chip and PIN payments.

Today’s businesses need flexible payment technology that can support:

Whether customers prefer to pay using Chip and PIN, tap-to-pay or mobile wallets, businesses benefit from having payment systems that can adapt to changing consumer behaviour.

Start accepting Chip & PIN, contactless and digital payments

Whether you're new to card payments or looking to switch providers, we can assist you. At Nomupay, we offer flexible in-store solutions to support modern payment methods, including Chip and PIN, contactless payments and digital wallets.. Whether you run a boutique shop, food truck or coffee business, we can help you make your passion pay.

Visit our in-store payments page for more information.