For many EU and US companies, expanding into Asia feels like the logical next step.

The region offers massive consumer markets, fast-growing economies and rising digital adoption. On paper, the opportunity looks enormous. Too good to miss!

But many Western businesses underestimate one critical reality: Asia is not a single market.

What works in Germany may still work in France with a few adjustments. What works in the US may transfer reasonably well to Canada or the UK.

Asia is different.

So many varying factors from country to country to consider, including consumer behaviour, regulations, payment systems, business culture, hiring expectations, language, the list goes on…

This is why many Western companies struggle after entering Asia, even when they have strong products, experienced leadership and proven success at home.

Let’s take a look at key factors you’ll need to consider to ensure you succeed in Asia too.

What’s in this blog:

- Asia’s fragmented market

- Localisation is essential

- Local payment methods

- Regulatory complexity

- Operational complexity

- How to succeed when expanding into Asia

1. Asia’s fragmented market

One of the biggest mistakes Western businesses make is treating Asia as a unified region.

Expanding into Japan is completely different from expanding into Malaysia. Selling to consumers in Indonesia requires a different strategy than targeting enterprise clients in Hong Kong.

Even neighbouring countries can have:

- different legal systems

- different social norms

- different preferred communication styles

- different purchasing behaviours

- different levels of digital maturity

And that’s not even covering the differences within the payments ecosystem.

A strategy that succeeds in one country may fail immediately in another. Companies that perform well in Asia focus on localisation rather than trying to copy-paste their Western playbook.

2. Localisation is essential

Many businesses assume localisation means translating their website into another language. In reality, this is just the start. What we really mean when we say localisation is adapting each touchpoint that will affect the consumer:

- pricing strategy

- marketing tone

- customer support

- hiring

- partnerships

- product design

- user experience

- currencies

- And potentially the most important, payment methods

Trust signals that work in Europe may not resonate with Asian consumers. The companies that succeed are usually the ones willing to adapt, not just translate.

3. Local payment methods

Let’s take a closer look at the importance of offering local payment methods.

In Europe and North America, card infrastructure is relatively mature and standardised, but this isn’t case across Asia. Why? Historically a large proportion of consumers were unbanked, resulting in low credit card adoption. Local payment methods were a great alternative to drive digital inclusion and commerce.

Customers frequently prefer:

- real-time payments

- domestic bank transfers

- QR-based payment systems

- local wallets

And these preferences vary country by country. For example, in Malaysia they prefer digital wallets like Touch ‘n Go and GrabPay, whereas in Indonesia, they’re more likely to use GoPay or OVO. It call comes down to trust and familiarity. If you don’t provide that, your conversion rate will feel the impact.

The amount of payment methods to choose from can be overwhelming, but doing your research beforehand to understand each market and their preferences will save you a lot of trouble further down the line.

To get you started, take a look at our local payment methods guide for Southeast Asia and Hong Kong.

4. Regulatory complexity

Payments expansion across Asia also introduces regulatory complexity that many businesses underestimate.

Licensing requirements, data handling rules, settlement structures and cross-border transaction regulations differ across the region.

Some countries are highly open to international payment providers. Others require:

- local entities

- domestic partnerships

- specific licenses

- local data storage

- in-country processing flows

Even basic operational questions become more complicated:

- Where can funds settle?

- Can merchants hold foreign currency?

- Are cross-border payouts restricted?

- What customer verification requirements apply?

A payments stack that works perfectly in Europe may require substantial restructuring in Asia. On top of that, you’ll need a dedicated team to stay on top of the local requirements to ensure you always remain compliant.

5. Operational complexity

The complexity doesn’t end with regulations. How your business operates day-to-day will bring its own unique complexities too.

Many Western businesses initially approach Asia as a single expansion project. But operationally, it often becomes multiple market entries at once.

Each country may involve:

- different acquiring relationships

- different settlement timelines

- different reconciliation flows

- different currencies

- different tax handling

Even customer support becomes more complex when payment disputes, refunds and failed transactions behave differently across markets.

This is one reason many companies underestimate the true operational cost and effort of regional expansion.

How to succeed when expanding into Asia

Now, it might seem like there are too many challenges to overcome and have you questioning whether it’s worth it. But we’re here to tell you that there is a way to take these challenges and simplify them.

Use a payment provider that can do it all under one roof!

Gone are the days where you need to use multiple PSPs to access multiple payments methods, or different systems to accept, payout and settle funds, or build multiple relationships with acquirers to be able to operate in each country.

Nomupay helps businesses simplify cross-border expansion by providing access to local payment rails, regional expertise and market-specific payment solutions across Asia.

For companies expanding from Europe or the US, you’ll get access to:

- local licences across the region for faster market entry

- 200+ local payment methods to build trust and improve conversion rates

- a single payout API so you can offer the complete end-to-end payment journey

- 180+ local currencies to accept payments and settle funds in

- local expertise on the ground to support with market trends, query support and navigating regional regulations

- a unified platform for complete visibility of your global data to track, manage and reconcile payments.

Successful expansion into Asia is rarely just about entering new markets. It’s about building an infrastructure that actually fits how those markets operate.

Want to learn more about how our global acquiring capabilities can support your expansion? Get in touch.

Malaysia is one of Southeast Asia’s fastest-growing digital payment markets, making it an exciting country, full of opportunity, to expand your business into.

With a highly digital-savvy population and strong government support for cashless initiatives, the country has rapidly shifted from cash-first to mobile-first payments.

If you want to succeed here, businesses need to take this market trend onboard and support a mix of e-wallets, real-time bank transfers, cards and QR payments to maximise conversion and meet local expectations. Ignoring it will only bring you more challenges.

That’s why we’re breaking it all down for you, covering the most important payment methods in Malaysia and how they impact your checkout strategy.

The Malaysian payments landscape

Before we dive into the payment methods, let’s take a closer look at Malaysia’s payment ecosystem. It has undergone a major transformation in recent years, rapidly moving away from cash. A study from Visa shows just how much digital payments now dominate.

Here are a few statistics to highlight this trend:

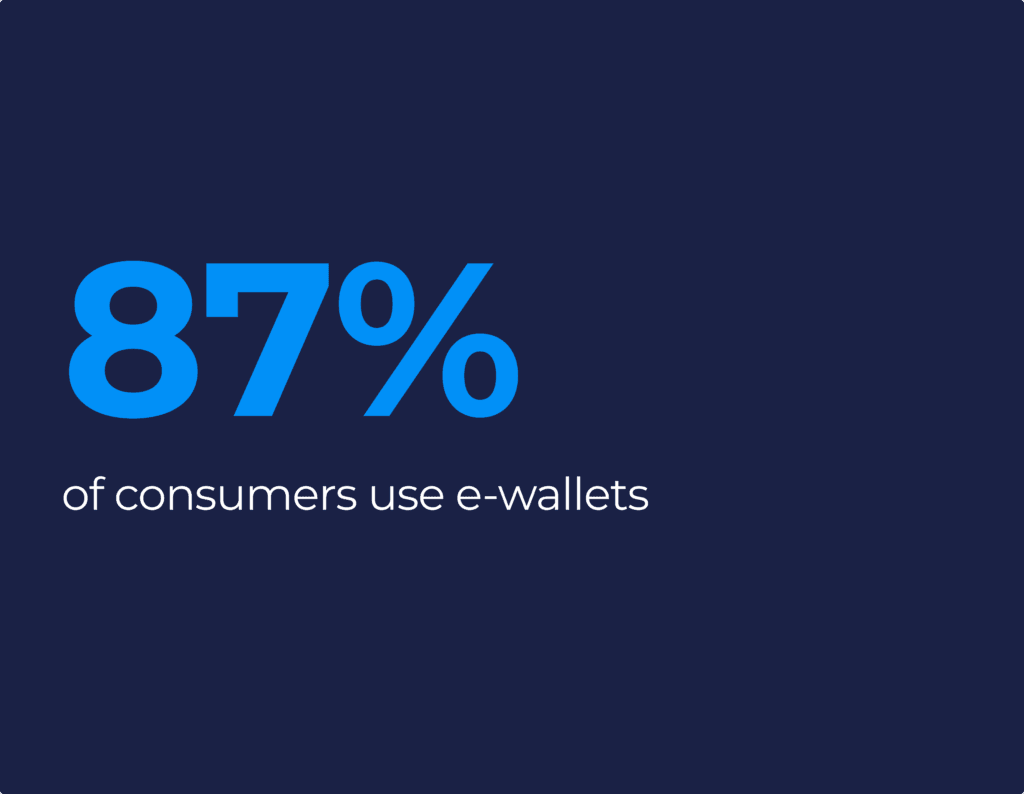

- Around 87% of consumers use e-wallets

- QR payments are used by ~68% of users, especially for everyday purchases

- 40% opt for using a virtual bank rather than a traditional bank

While cash is still used in rural areas and small businesses, digital payments are taking over in urban commerce, ecommerce and mobile-first transactions.

For merchants, this means one thing: Local payment method support is essential for conversion.

Key trends shaping payments in Malaysia

- Mobile-first behaviour - Consumers increasingly shop and pay via smartphones, making mobile optimisation essential.

- QR-first infrastructure - Malaysia has leapfrogged traditional POS systems, with QR codes becoming a primary payment method.

- Wallet-driven incentives - Cashback, rewards and promotions heavily influence payment choice.

- Fragmented but interoperable ecosystem - With 30+ active e-wallet providers, Malaysia is competitive, but unified systems like DuitNow QR create interoperability.

The most popular payment methods in Malaysia

1. E-wallets (digital wallets)

As the stat above shows, e-wallets are the leading payment method in Malaysia, particularly among younger consumers and mobile-first users.

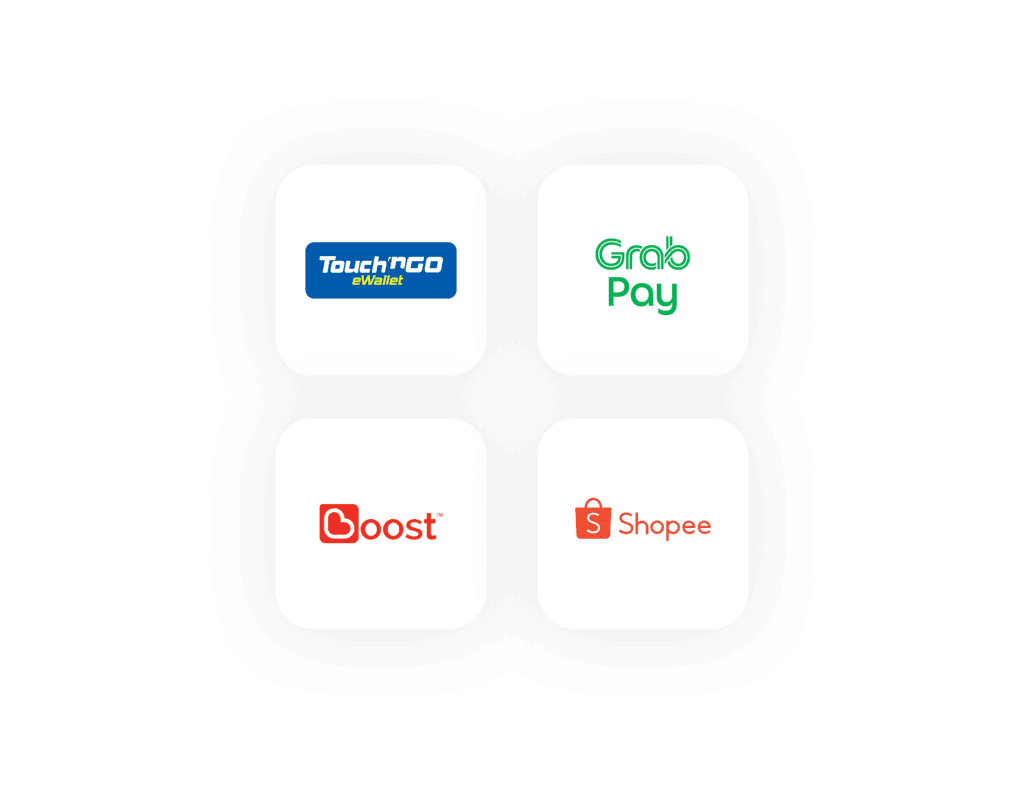

Popular options include:

- Touch ‘n Go

- GrabPay

- Boost

- ShopeePay

These wallets allow users to pay via QR codes, in-app payments or contactless NFC.

Why they matter:

- Fast checkout (especially on mobile)

- Cashback, rewards and promotions drive usage

- Widely accepted across online and offline merchants

GrabPay alone has over 100 million users across Southeast Asia, so it’s a no-brainer to offer this e-wallet to help you gain trust across the region.

Simply put, if you don’t offer e-wallets, you risk losing a significant share of transactions.

2. QR payments (DuitNow QR)

QR payments were dominating the region way before the West adopted the method during COVID-19, and is still a defining feature of Malaysia’s payment ecosystem.

The national standard, DuitNow QR, allows users to pay using any participating bank or wallet app by scanning a single QR code.

Common use cases:

- Street food vendors and night markets

- Cafés and small retailers

- Ride-hailing and delivery

Why they matter:

- Low cost for merchants (no POS terminal needed)

- Extremely fast checkout

- Works across banks and wallets

QR codes will be spotted everywhere across retail environments, from small stalls to large chains.

3. Account-to-account (A2A) payments

Bank transfers remain a core, trusted payment method, especially for higher-value purchases.

Key systems include:

- FPX (Financial Process Exchange) – widely used for ecommerce

- DuitNow transfers – real-time bank-to-bank payments

Why they matter for consumers:

- Trusted and familiar

- Real-time processing

- No need for card details

Why they matter for merchants:

- Lower fees than cards

- Instant settlement

- No chargebacks

FPX is considered one of the most popular online payment methods in Malaysia for secure, high-value items. Whereas DuitNow is much more widely used for day-to-day transactions. So depending on your business model and what service you’re providing will determine which method is more suitable for you.

4. Cards (credit & debit)

It is important to note that cards are still widely used, so you don’t want to disregard them completely, particularly for:

- Supermarkets and retail chains

- Petrol stations

- Travel and international payments

Contactless “tap-and-go” payments are standard across most terminals.

Although cards are no longer dominant, especially for smaller transactions due to the rise of e-wallets and QR payments, diversity is key to ensure you cover all consumer preferences.

5. International payment methods

Let’s not forget the big global payment methods too.

For cross-border commerce, Malaysians also use:

- PayPal

- Apple Pay / Google Pay

- International cards (Visa, Mastercard)

- Multi-currency wallets

Common use cases:

- Travel

- Cross-border ecommerce

- Subscriptions

It’s likely that you’ll already have at least one of these payment methods integrated into your checkout so are an easy win. But, you can’t rely on these alone. Offering these as part of a wider choice alongside local payment methods is what will set you apart from your competitors.

What payment methods should you offer in Malaysia?

There are plenty of options to choose from, so which one should you choose for your business? We know it may not be realistic to say all of them, so to really succeed in Malaysia, here are a few considerations to think about when choosing which payment method to offer:

- Your consumer base – Are you targeting a younger, digital-savvy audience or an older generation?

- Your business model – What service are you providing? Is it high-value?

- Compatibility – What system are you using and which APMs is it compatible with?

- Resource – How many APMs can your business manage?

- Regulatory compliance – Each payment method has its own regulations; can you stay on top of them?

Considering these points carefully is crucial to ensure you offer the right mix of local payment methods to increase conversion rates, reduce cart abandonment and improve customer experience.

Final thoughts

To wrap up, Malaysia’s payment landscape is fast, mobile and highly localised. E-wallets and QR payments dominate everyday spending, while bank transfers and cards still play important supporting roles.

For businesses, success comes down to one principle: Offer the payment methods your customers already use. In Malaysia, that means prioritising wallets, QR and real-time bank payments, not just cards.

If it’s not just Malaysia that you’re expanding into, and want to know more about the landscape of Southeast Asia, take a look at our local payment methods guide.

For years, digital publishing has relied heavily on a one-size-fits-all model: the monthly subscription. While this approach has driven predictable recurring revenue, it no longer reflects how readers actually consume content.

Today’s audiences want flexibility. They don’t just “subscribe”; they dip in, binge, follow events, read seasonally and then drop off when they no longer find value in the content.

For digital publishing platforms, from e-books to journalistic web pages and educational content, the opportunity is clear: move beyond fixed monthly subscriptions and build flexible plans that match real reading behaviour.

Done well, flexibility doesn’t reduce revenue. It increases conversion, retention and lifetime value.

What’s in this blog:

- Why the traditional subscription model is showing its limits

- Flexible monetisation models that increase conversion

- Why flexibility increases revenue (not reduces it)

- Reducing friction at checkout

- The role of payment infrastructure in enabling flexibility

Why the traditional subscription model is showing its limits

The monthly subscription model for digital publishing companies assumes users consume content consistently every month and that there are only two options: subscribe or churn.

In reality, reading behaviour is far more irregular.

A user might:

- Binge-read during holidays

- Subscribe for a single series or author

- Engage heavily around specific news cycles or events

- Want temporary access without long-term commitment

When the pricing structure doesn’t match usage patterns, users often opt out entirely rather than commit.

That’s where flexibility becomes a part of your growth strategy.

Flexible monetisation models that increase conversion

If the traditional method is no longer working for today’s consumer base, then what are the options?

1. Day passes and short-access tickets

Not every user wants a subscription. Some just want access now.

Day passes or 24-hour access models allow users to access the content they want during a specific moment of interest and to try the platform with minimal commitment.

This model works particularly well for:

- News platforms during breaking events

- Academic or reference content

- E-book discovery or “try before you commit” journeys

Although this type of reader are not bringing in recurring revenue right away, you could miss out on a large audience base and, therefore, revenue, if you don’t offer this little to no commitment plan.

2. Event-based or content drops

Instead of selling time-based access, online publishing platforms can sell moment-based access.

For example:

- Content on current elections

- Seasonal reading collections

- New releases

This aligns monetisation with intent, not just time. It also creates urgency, a powerful driver of conversion.

3. Flexible subscriptions

Monthly billing is often the default, not the optimal choice.

Offering alternatives such as weekly subscriptions or quarterly or annual plans can significantly improve acquisition by reducing psychological friction and provide options that suit the readers lifestyle or financial situation.

Even when lifetime value remains similar, removing the “monthly lock-in” perception can lift conversion rates.

4. Pause instead of cancel

One of the most effective retention tools is surprisingly simple: the ability to pause subscriptions.

There are many reasons why a user may want to cancel, for example, they could be travelling or temporarily time poor, and they don’t want to waste their money on a service they can’t currently use.

In situations like these that are temporary, a pause option is much more beneficial. This small feature can meaningfully reduce churn.

5. Usage-based bundles and credit systems

For platforms with mixed content types, prepaid credit systems can be powerful.

For example, you could allow your users to:

- Buy credits to spend on articles, e-books or premium access

- Bundle credits with expiry windows or bonuses

- Rollover or gift credits

This decouples payment from rigid time periods and instead aligns it with actual consumption.

Why flexibility increases revenue (not reduces it)

At first glance, more flexible pricing might seem like it risks lowering ARPU. It may seem counterproductive to allow your readers to pause subscriptions or only drop in now and then, but in practice, it often does the opposite.

Flexibility drives:

- Higher conversion – If a consumer is unsure whether to commit or not, having that flexibility may just convince them to go for it.

- Lower churn - Users don’t feel trapped and are more likely to stick around if they can make the subscription work for them with pricing that matches their usage patterns.

- Better reactivation rates – By being able to pause, you’re making it easier for them to return.

- More upsell opportunities – With event-based or bundle upgrades, you can offer great deals to increase conversions even more.

The result: a healthier revenue mix across short-term and long-term users.

Reducing friction at checkout

Although these flexible pricing options are worthwhile, they only only work if payment friction is low too. Long-winded checkout flows and payment failures will put anyone off continuing with your service.

A smooth checkout needs:

- Seamless card registration with minimal fields to fill out

- Secure stored payment methods for returning customers

- Smart retries for failed payments

- Easy upgrades, downgrades and plan switching

- Clear billing transparency

Without these, it doesn’t matter how flexible your service is; payment friction kills conversion.

The role of payment infrastructure in enabling flexibility

Behind every successful, flexible monetisation model is a strong payments foundation.

Platforms need systems that can:

- Handle multiple pricing structures in parallel

- Support dynamic subscription plans (active, paused, upgraded, expired)

- Manage recurring billing with minimal failure rates

- Reconcile missed/failed payments quickly

- Ensure compliance, security and trust at scale

This is where modern payment providers play a critical role, not just processing transactions, but enabling product strategy.

The most successful digital publishers are increasingly treating payments as a core part of the user experience, not a back-office function.

To summarise:

Digital publishing is shifting from static subscriptions to dynamic access models.

Readers don’t want to be locked into a single monthly commitment. They want control and flexibility in how they pay for content.

The next wave of growth in digital publishing won’t come from raising subscription prices. It will come from rethinking how access itself is monetised.

If you’re ready to upgrade your subscription model, take a look at how our solutions package is built for digital publishing platforms like yours.

The travel industry is one of the most globalised sectors in the world. But behind every booking is a complex payments journey.

From cross-border transactions and multiple currencies to high chargeback exposure and long booking windows, travel businesses face unique payment challenges that many providers aren’t built to handle.

That’s why choosing the right merchant account for travel isn’t just a technical decision — it’s a growth decision. The right setup can improve approval rates, reduce risk and support international expansion.

What’s in this blog:

- What is a travel merchant account?

- Why is the travel industry classed as high-risk?

- How can travel businesses reduce risk and chargebacks?

- Why global payment capabilities matter in travel

What is a travel merchant account?

A travel merchant account is a type of payment processing solution designed specifically for businesses operating in the travel sector.

This includes:

- Online travel agencies (OTAs)

- Tour operators and travel agencies

- Hotels and accommodation providers

- Car rental companies

- Airlines, cruise lines and transport providers

- Holiday packages

- City tours

However, keep in mind that there could be other travel business models not mentioned in the list above.

In simple terms, it allows travel businesses to accept and process payments online, often across multiple countries and currencies, while managing the higher levels of risk that go hand-in-hand with the industry.

Unlike standard merchant accounts, travel payment processing requires additional considerations such as fraud prevention, chargeback management and international payment acceptance.

Why is the travel industry classed as high-risk?

Travel is considered a high-risk industry by many acquiring banks and payment providers globally, not because it’s unstable, but because of how it operates at scale. These are the main reasons why:

- High cancellation rates: Travel plans can change quickly. Whether due to personal circumstances or global events, cancellations are common and often lead to refunds or disputes.

- Long booking windows: Customers frequently pay weeks or months in advance. This creates a longer exposure period where something can go wrong or the customer could change their mind, increasing the likelihood of chargebacks.

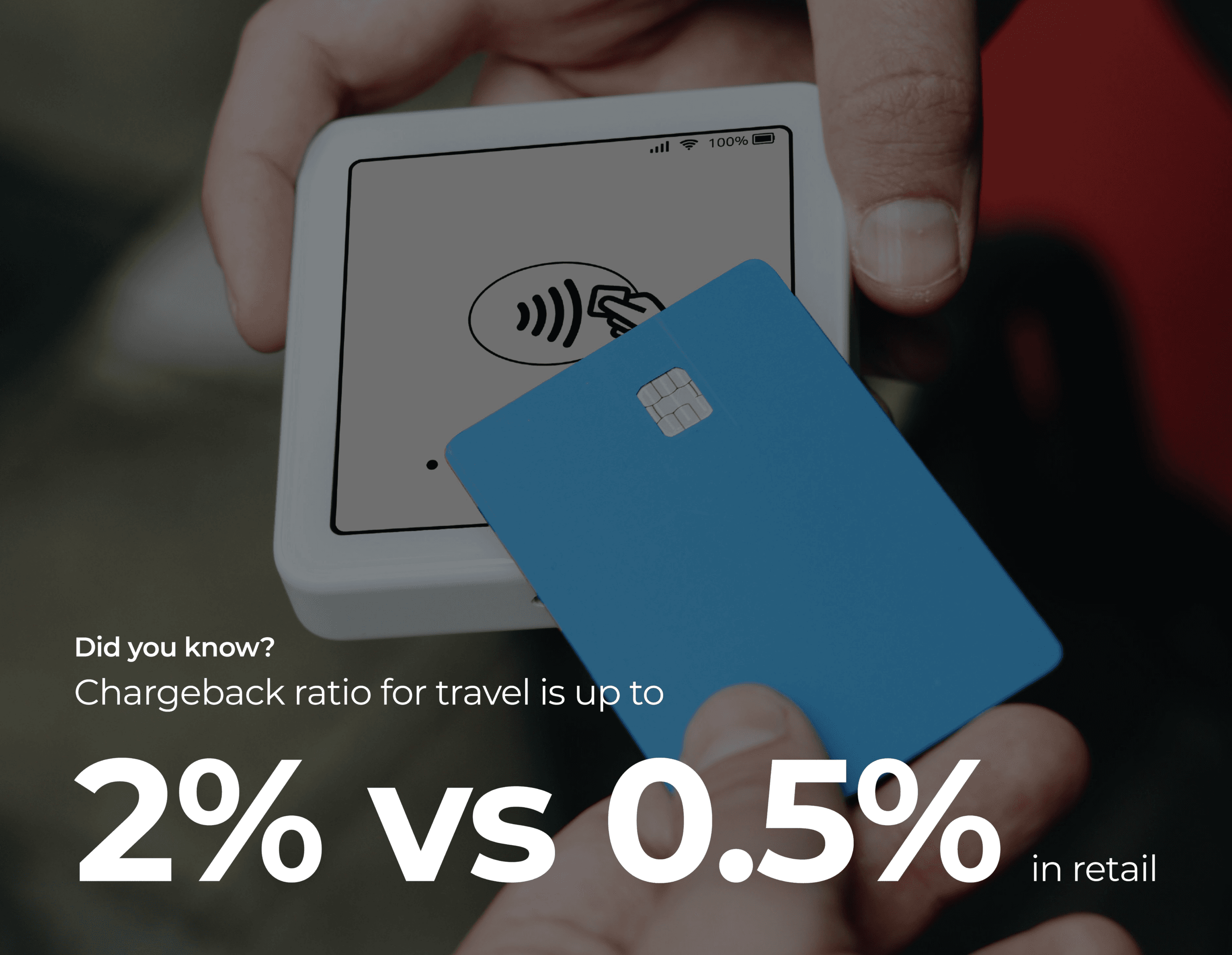

- High transaction values: Travel purchases are typically higher in value than standard ecommerce transactions, which inevitably increases both fraud risk and financial exposure.

- Chargeback behaviour: Many travellers go directly to their bank instead of requesting a refund, often because they don’t understand the difference between a chargeback and a refund. This leads to higher chargeback ratios.

- Cross-border complexity: Travel payments are inherently international. A customer in one country may book a service in another, using a card issued elsewhere, adding layers of fraud risk, compliance requirements and approval challenges.

- Currency and FX exposure: Handling multiple currencies can become an operational headache with inconsistent pricing experiences and additional risk if not managed correctly.

How can travel businesses reduce risk and chargebacks?

All online businesses should be aware of the possible risks when selling online. That’s why we recommend that all online merchants adopt at least the basic fraud protection measures. Accordingly, high-risk businesses should be extra vigilant and take additional fraud protection measures if necessary.

Here are a few tips which can help prevent fraud and minimise the risk of chargebacks:

- Work with a specialist payment provider: Choose a partner with experience in travel payment processing and high-risk industries. They should understand the nuances of travel business models and offer tailored support with an experienced risk management team and comprehensive fraud tools.

- Leverage global acquiring: Access to local acquiring in key regions (such as the EU and APAC) can improve authorisation rates, reduce cross-border fees and minimise false declines.

- Implement strong authentication (3D Secure): Integrating 3D Secure is a must for every high-risk online business. It is an extra layer of protection in the payment process by verifying the customer’s identity, helping reduce fraud and shift liability away from the merchant.

- Monitor transactions proactively: Always monitor transactions and look out for any inaccuracies or red flags to prevent fraud before it escalates.

- Prioritise customer support: Fast, responsive customer service can significantly reduce chargebacks. If customers can easily request refunds or changes, they’re less likely to go to their bank.

- Stay ahead of industry trends: Payments and fraud tactics evolve quickly. Staying informed helps you adapt and protect your business. Nomupay's blog could be a great place to start – We have prepared a bunch of informative articles about fraud prevention and chargebacks, all of them can be found here.

Why global payment capabilities matter in travel

Travel businesses don’t operate in a single market — and neither should their payments.

Customers expect to:

- Pay in their local currency

- Use their preferred payment method

- Experience a smooth, frictionless checkout

Without the right international payment processing setup, businesses may face:

- Lower approval rates for international cards

- Higher processing costs

- Increased fraud and false declines

- Poor customer experience at checkout

A global acquiring strategy helps solve this by enabling:

- Better acceptance rates across regions

- Localised payment experiences

- More efficient cross-border transactions

For travel merchants looking to grow internationally, this isn’t optional, it’s essential.

Final thoughts

The travel industry presents huge opportunities, but also unique payment challenges.

From managing chargebacks to navigating cross-border transactions, having the right travel merchant account in place can make a significant difference to both performance and scalability.

For businesses expanding internationally, payment infrastructure becomes a key competitive advantage.

At Nomupay, we work with travel merchants to:

- Improve payment acceptance rates

- Reduce chargeback risk

- Enable seamless cross-border payments

- Support global growth

If you’re looking to optimise your payment setup or expand into new markets, it may be time to rethink your approach to payments. Get in touch!

Nomupay and TProfile join forces to provide embedded seamless payments for global travel brands.

We’re excited to announce a new partnership with TProfile, an award-winning travel quotation and booking platform. The collaboration will enable travel companies including retail, homeworking, tour and cruise operators to seamlessly embed payment processing directly into their booking flows, enhancing customer experience and creating new opportunities for revenue growth.

Localised experience through a single integration

Through this partnership, TProfile will integrate Nomupay’s payment solutions, allowing customers to pay travel deposits and balances securely via cards, digital wallets (Apple Pay, Google Pay), Pay by Bank and local alternative payment methods (APMs). This unified integration eliminates friction in the payment process and gives online travel agencies and travel advisors the flexibility to offer multiple payment options, all from within their TProfile-powered platform.

Tony Evans, CEO of TProfile, said: “Our clients have been asking for a seamless, integrated payment experience that matches the quality of their booking and quotation journeys. Partnering with Nomupay allows us to provide exactly that and more — a secure, efficient and globally scalable payments solution that enhances customer trust and conversion using multiple payment methods. Importantly, for those businesses that want to use a monthly payment option, TProfile also facilitates pre calculation of monthly payments in line with the balance due dates, creating an easy pay method for customers.”

Powering global expansion

Nomupay’s acquiring network provides a global reach that ensures that TProfile’s customers, from boutique travel advisors to enterprise-level operators, can accept and manage payments across multiple regions through a single integration.

Paul Farquharson, Head of Partnerships at Nomupay, said: “TProfile has transformed how travel brands communicate and sell, combining beautiful customer engagement with powerful automation. By embedding Nomupay’s payment rails, we’re helping travel businesses reduce operational complexity, accelerate cash flow and deliver a truly modern payment experience to their clients.”

Together, we share a common vision of supporting innovation in the travel sector, empowering travel brands with technology that simplifies operations, drives efficiency and strengthens customer relationships.

Subscriptions are the lifeline of streaming platforms. Whether you run a video streaming platform, music streaming platform or one of the many fast-growing gaming streaming platforms, recurring revenue is what keeps your business predictable and scalable.

But here’s the challenge: not all subscription payments that fail are truly “lost”.

In fact, a significant portion of failed payments can be recovered if you have the right tools in place.

This is where many streaming platforms are leaving money on the table.

What’s in this blog:

- Why subscriptions fail in the first place

- How to recover payments

- Turning payment failures into growth

Why subscriptions fail in the first place

Before we talk about recovery, it’s important to understand why subscriptions fail. Most failures aren’t due to customer intent; they’re caused by avoidable payment issues such as:

- Expired or replaced cards

- Insufficient funds at the time of billing

- Bank declines or authorisation errors

- Customers switching payment methods without updating details

For streaming media platforms operating at scale, even a small percentage of failed payments can quickly translate into significant revenue loss.

The good news? Many of these failures are recoverable.

How to recover payments

When a payment fails, the default response for many platforms is to cancel access or prompt the user to re-subscribe manually.

But this approach creates friction, and often results in churn.

Modern streaming platforms are shifting toward proactive recovery strategies that work in the background, improving the customer experience while protecting revenue.

Let’s break down how.

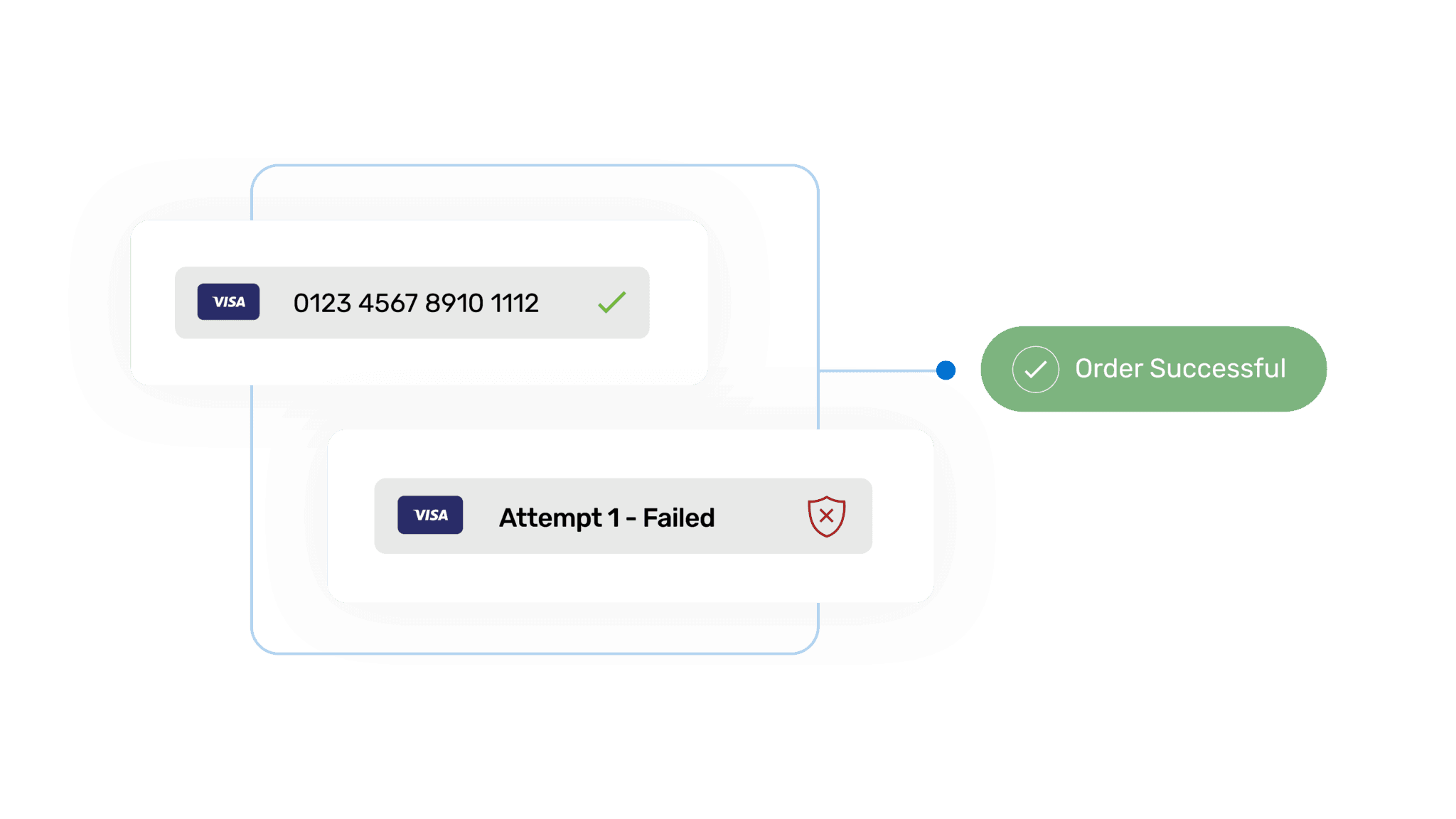

1. Smart reconciliation with auto-retries

Not all payment failures are permanent. In many cases, a simple retry at the right time can successfully process the payment. With optimum billing data, the payment can be taken again later that day or the following day, rather then being retried immediately. Why? Well, if a payment has been declined due to “insufficient funds”, the situation won’t change moments later.

This kind of intelligent retry logic can significantly increase recovery rates without any customer intervention.

2. Multi-card registration

Customers today often have multiple payment methods. If their primary card fails, they may still be willing (and able) to pay, but only if given the option.

Multi-card registration allows users to:

- Store backup cards securely

- Automatically switch to an alternative payment method if the primary fails

For video streaming platforms and music streaming platforms with global audiences, this flexibility can make a substantial difference in reducing involuntary churn.

3. Automatic card updates

One of the most common reasons for failed subscriptions is outdated card information.

Cards expire. They get lost. They get replaced.

Automatic card update services solve this by updating card details in real time through card networks, ensuring subscriptions continue without interruption.

This means fewer failed payments and fewer unnecessary cancelled subscriptions.

4. Recover revenue with pay-by-links

Sometimes, automation isn’t enough, and that’s where direct customer engagement comes in.

Pay-by-link allows you to:

- Send a secure payment link via email or SMS

- Let customers quickly update or complete their payment

- Recover subscriptions without requiring full re-registration

This is particularly useful for live streaming platforms where timing matters, for example, when users want immediate access to an event.

5. Flexible billing schedules

Circumstances change, things come up and, sometimes, that can effect cash flow. By not providing any flexibility to accommodate this, you could risk losing the customer all together.

Flexible scheduling gives you the ability to:

- Pause subscriptions instead of cancelling them

- Adjust billing dates to better align with customer cash flow

- Offer grace periods without disrupting access

This approach is especially valuable for gaming streaming platforms and other services with fluctuating usage patterns.

Turning payment failures into growth

The most successful streaming platforms don’t treat failed payments as the end of the customer journey. They treat them as a recovery opportunity by utilising the solutions mentioned above.

Let’s recap:

- Intelligent retries

- Multiple payment options

- Real-time card updates

- Frictionless recovery tools like pay-by-link

- Flexible subscription management

By combining the tools you can significantly reduce involuntary churn and discover hidden revenue.

But delivering this kind of recovery strategy at scale isn’t something you can do alone.

Not all payment providers are built to support the complexity of modern streaming media platforms. To truly recover lost subscriptions, you need a partner that understands:

- Recurring billing at scale

- Global payment behaviours

- Customer experience across different streaming models

A strong payment partner doesn’t just process transactions — they actively help you protect and grow your subscription revenue.

Final thoughts

In a competitive market where users can switch platforms in seconds, every recovered subscription counts.

The difference between losing a customer and retaining one often comes down to what happens after a payment fails.

With the right recovery strategies in place, streaming platforms can turn payment failures into a seamless experience and a powerful growth lever.

If you’re looking to improve subscription recovery and reduce churn, it may be time to rethink your payments strategy.

Southeast Asia is rapidly becoming one of the most dynamic payments markets in the world. So, if you’re not already considering expanding into the region…why not? For merchants in Europe and the United States with expansion into the region on their roadmap, it’s important you understand its unique infrastructure.

At the centre of its growth is the rise of real-time payment systems, supported by a distinctly wallet-first consumer behaviour, Government-led innovations and the increasing cross-border connectivity. Together, these forces are reshaping how money moves across the region and redefining what a successful checkout experience looks like.

A region built for real-time payments

Across Southeast Asia, governments and central banks have invested heavily in real-time payment rails. Systems such as PayNow in Singapore, PromptPay in Thailand and DuitNow in Malaysia have made instant bank-to-bank transfers a standard part of everyday commerce.

For consumers, this means payments that settle in seconds rather than days. For merchants, it offers faster access to funds, lower transaction costs and a credible alternative to traditional card networks.

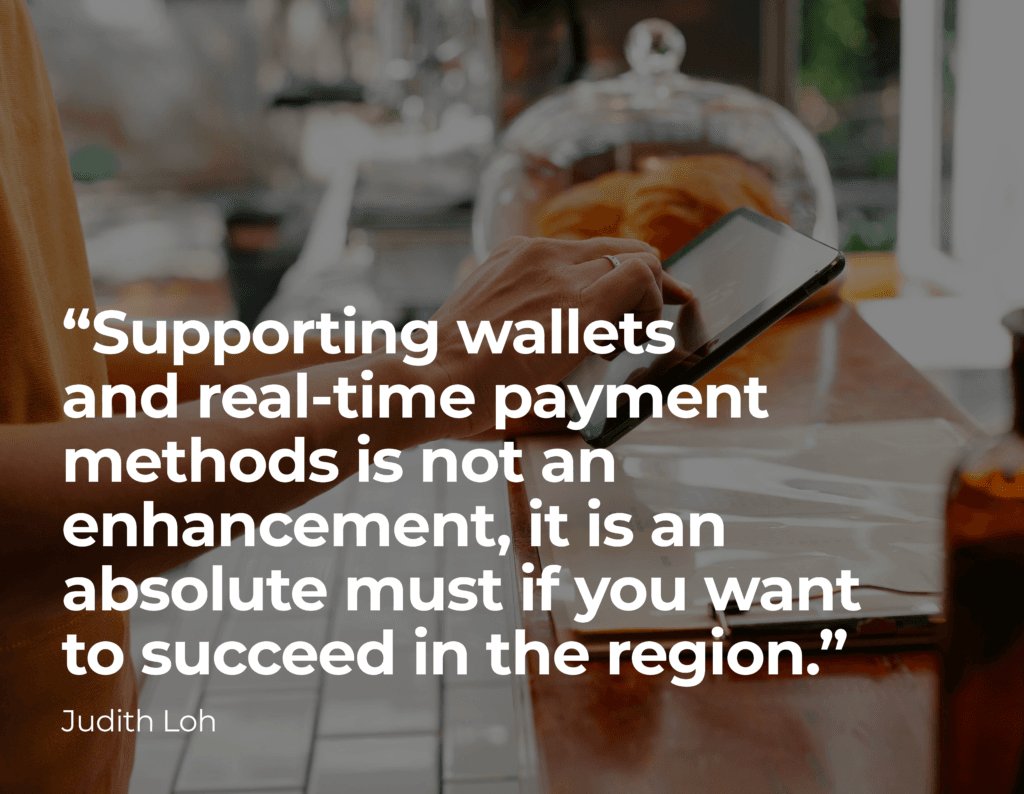

Judith Loh, Nomupay’s SVP Sales for APAC, says: “What makes Southeast Asia particularly interesting to me is its pace of adoption. In many ways, the region has skipped a generation and moved straight from cash to real-time, mobile-first systems, bypassing traditional card infrastructure altogether. You can see that play out more broadly across APAC too where digital wallets made up 77% of ecommerce and 63% of POS value last year.”

This has created a payments environment that is not only modern, but structurally different from Western markets.

The wallet-first reality

To understand real-time payments in Southeast Asia, it is essential to recognise that consumers do not default to cards. Instead, mobile wallets and bank-linked apps sit at the centre of the payment experience.

Wallets such as GrabPay, GoPay and ShopeePay are deeply embedded in everyday life, from transport and food delivery to bill payments and peer-to-peer transfers.

The real-time payment infrastructure underpins many of these wallets. Users can top up instantly, transfer funds seamlessly and pay merchants via QR codes or in-app flows. The distinction between a bank transfer and a wallet payment is often invisible to the consumer.

For Western merchants, this creates a critical challenge. A checkout experience optimised for cards will feel unfamiliar and potentially inconvenient to local consumers.

“Supporting wallets and real-time payment methods is not an enhancement, it is an absolute must if you want to succeed in the region.” – Judith Loh

QR codes as a universal payment method

Many Western merchants were introduced to QR codes during COVID-19, when contactless experiences became a necessity. While some have continued to offer QR-based payments, others have largely reverted to pre-pandemic habits.

In Southeast Asia, however, the story is very different. QR codes were already gaining traction well before the pandemic and have since become a core part of the payments landscape rather than a temporary solution.

In markets such as Indonesia, Thailand and Singapore, QR payments now function as a universal acceptance method. From large retailers to small street vendors, merchants can accept payments by displaying a single QR code that connects to multiple wallets and bank apps. This has significantly lowered the barrier to digital acceptance and accelerated the shift away from cash.

For international merchants, QR-based payments represent more than just an additional option. They are an opportunity for a low-cost route to broad market access, but they also require rethinking the checkout experience, particularly in mobile and cross-border contexts.

Connecting payments across borders

Perhaps the most significant development is the growing connectivity between national real-time payment systems. Countries across ASEAN are actively linking their domestic schemes, allowing users to send money across borders using familiar apps and local currencies.

For example, connections between Singapore’s PayNow and Thailand’s PromptPay enable cross-border transfers that are near-instant and far cheaper than traditional international payments. Similar linkages are emerging between Malaysia, Indonesia and other markets in the region.

“I can’t stress enough how important this is for cross-border commerce. It reduces reliance on international card networks and correspondent banking, lowers foreign exchange costs and simplifies the payment experience for regional consumers.” – Judith Loh

In practical terms, a customer in Bangkok can increasingly pay a merchant in Singapore using their domestic banking app, without needing a card or navigating complex international payment flows.

What this means for western merchants

For merchants entering Southeast Asia, the rise of real-time payments is not just a technical detail. It is a strategic consideration that affects conversion, cost and customer experience.

First, localisation is essential. Supporting local payment methods, particularly wallets and real-time bank transfers, is key to reaching customers in each market.

Second, speed matters. Real-time settlement can improve cash flow and reduce operational friction, but it also requires adjustments to reconciliation, refunds and risk management processes.

Third, cross-border is being redefined. As regional payment systems become more interconnected, merchants have an opportunity to serve customers across multiple markets with fewer intermediaries and lower costs.

Finally, partnerships are critical. Navigating the fragmented landscape of payment methods, regulations and infrastructure often requires working with local payment providers or global platforms that aggregate these capabilities.

A new payments paradigm

“Southeast Asia offers a glimpse into the future of payments. It is a region where real-time infrastructure, mobile wallets and cross-border connectivity are converging to create a faster, more inclusive and more efficient system.” – Judith Loh

For Western merchants, success will depend on recognising that this is not simply an extension of existing payment models. It is a fundamentally different paradigm, shaped by local behaviours and government-led innovation.

Those who adapt to this reality will not only unlock growth in Southeast Asia, but also gain insights that may well shape their global payments strategy in the years ahead.

Looking to enter into the Southeast Asia market? Learn more about the market trends and customer preferences from our Local Payment Methods guide, or get in touch to see how we can help you achieve your expansion goals.

If you're a digital content creator, chances are you’ve spent hours perfecting your content, but far less time thinking about how you actually get paid.

And that’s completely normal.

As much as you want to get paid, the payments infrastructure isn’t the exciting part of building a digital business. But they are the foundation of turning your creativity into sustainable income. Get them wrong, and you risk losing revenue, frustrating your audience or limiting your growth.

Let’s walk through the most common mistakes content creators make when setting up payments, and how to fix them.

1. Overcomplicating the payment experience

One of the biggest mistakes in digital content platforms is adding too much friction to the checkout process.

You don’t need to know every little detail about your customer. And you don’t need to make them sign up to an account. Long forms, too many steps or limited payment options can cause potential customers to drop off before completing a purchase.

Why it matters:

In digital entertainment, impulse often drives purchases. If the process isn’t seamless, users simply won’t follow through.

How to fix it:

- Keep checkout simple and mobile-friendly

- Offer popular payment methods (cards, wallets, local options)

- Minimise required fields and offer guest checkouts

The easier it is to pay, the more likely users will convert.

2. Ignoring global audiences

Digital media content has no borders, but many creators still set up payments as if their audience is local.

A digital business needs to be treated very differently to a little pop-up shop in your local town. You could be filming your content in the UK, and have viewers over in Hong Kong.

Why it matters:

If you're building a digital content as a service model, your audience could be anywhere in the world. Limiting currencies or payment methods means leaving money on the table.

How to fix it:

- Accept multiple currencies

- Support region-specific payment methods

- Be transparent about pricing across markets

Think global from day one, even if your audience starts small.

3. Not planning for recurring revenue

Many creators focus only on one-time purchases, missing out on the stability of subscriptions.

Now, I know we said above about offering guest checkouts, but the point is, your customers need options. If they’re loyal and keep coming back to your content, a subscription service is the ideal solution for both them for ease and you for recurring revenue.

Why it matters:

Recurring payments are the backbone of a sustainable digital business. They provide predictable income and increase customer lifetime value.

How to fix it:

- Offer subscription tiers (monthly, yearly)

- Keep them flexible - make it easy to upgrade, downgrade or cancel

- Clearly communicate value at each level

Subscriptions turn casual buyers into loyal fans.

4. Poor pricing strategy

Pricing digital content is tricky. Charge too much and you scare users away. Charge too little and you undervalue your work.

Do your research beforehand to see what other creators are charging. There may be a bit of trial and error at the beginning, but it’s an important factor to get right.

Why it matters:

Your pricing signals quality and shapes how your audience perceives your brand.

How to fix it:

- Test different price points

- Offer bundles or tiered access

- Consider freemium models to attract new users

Pricing isn’t static. Treat it as something you refine over time.

5. Overlooking payment failures

Failed payments are more common than most creators realise and often go unmanaged.

There are multiple reasons for failed payments, and it’s not always because the customer doesn’t have enough funds. Being able to access tools from your payments provider to prevent and manage failed payments will be invaluable to your bottom line.

Why it matters:

In subscription-based digital content platforms, failed payments directly impact revenue and retention.

How to fix it:

- Set up automatic retries

- Notify users clearly and quickly

- Use smart recovery tools (like multi-card registration or automatic card updates)

Recovering failed payments is often easier than acquiring new customers.

6. Lack of transparency with fees

Hidden fees or unclear pricing can damage trust quickly. Nobody likes to see one price, and then get stung with a larger bill at the end.

Why it matters:

Trust is everything in digital media content. If users feel misled, they won’t come back.

How to fix it:

- Clearly display the total cost upfront

- Avoid surprise charges at checkout

- Communicate taxes or platform fees transparently

Transparency builds long-term loyalty.

7. Not thinking about scale

What works for your first 10 customers might break when you have 10,000. It can take time to build a digital business, but with the way the digital world works, you never know when you’re business is going to grow.

All it takes is one viral piece of content to take you from a small audience one day, to a global phenomenon the next – and you need to be ready for it!

Why it matters:

As your digital content platform grows, your payment system needs to grow with you.

How to fix it:

- Choose a scalable payment infrastructure early

- Automate reporting and reconciliation

- Ensure your system supports high transaction volumes

Planning for scale saves major headaches later on.

8. Treating payments as an afterthought

This is the root of most problems. Creators often focus on content first and bolt on payments later leading to inefficiencies and missed opportunities.

The payments system is what takes your content from being a hobby to a paid job. If you want to be a content creator full time, then you need to make payments part of your strategy.

Why it matters:

Payments aren’t just operational; they’re part of your user experience and growth strategy.

How to fix it:

- Integrate payments into your overall business model

- Align pricing, packaging and payment flows

- Regularly review and optimise performance

The best content creators treat payments as a core part of their digital business.

Final thoughts

Whether you're building a digital content platform, launching a subscription service or monetising digital entertainment, your payment strategy can make or break your success.

The good news? Most of these mistakes are fixable.

By simplifying the experience, thinking globally and planning for growth, you can turn payments from a pain point into a powerful advantage.

And that’s when your digital content truly starts working for you.

Take a look at our page dedicated to your industry and let’s see how we can help you take your digital platform to the next level.

Hong Kong has always been a city where tradition meets innovation, and its payment landscape is no exception. From the popular Octopus card to a booming digital wallet scene, consumers here move fast, shop smart and expect seamless checkout experiences both online and offline.

If you’re a business looking to grow in Hong Kong, understanding how people pay can make a huge difference to your success. Let’s take a look at the how the market has evolved and which online payment methods you need to focus on.

What’s in this blog:

- Hong Kong’s payment evolution

- The rise of contactless at Point of Sale

- Today’s market trends

- The payment methods businesses must offer in Hong Kong

- What this means for businesses

Hong Kong’s payment evolution

Hong Kong is known for its highly developed digital infrastructure and tech-savvy consumers. While the Northeast Asia region has long been a leader in e-commerce and sophisticated cross-border trade, Hong Kong has carved its own path when it comes to payments.

Historically, cards have dominated, and they’re still incredibly important today. Credit cards remain a trusted way to pay for everything from online shopping to dining out. But over the last few years, the city has experienced a strong push toward cashless, mobile-first payments, helped by government-supported digital initiatives and changing consumer habits.

The rise of cashless at Point of Sale

Across Northeast Asia, governments have encouraged the shift toward digital payments to reduce the reliance on cash, expand financial inclusion and support economic growth. Hong Kong has followed this trajectory with physical retail now seeing rapid adoption of contactless, QR-based and wallet-driven payments.

Today’s market trends

Here’s what’s influencing how Hong Kong shoppers choose to pay right now:

1. A contactless culture

Hong Kong embraced contactless payments long before many other markets. Octopus paved the way, making “tap-and-go” behaviour second nature. That expectation now extends to mobile wallets and cards.

2. Growth of mobile wallets

Mobile payments have surged, especially among younger shoppers and commuters. Many consumers now prefer the speed and convenience of wallets linked to their phones, prepaid cards or bank accounts.

3. Cross-border shopping

With strong trade and cultural ties to mainland China, Hong Kong consumers are increasingly comfortable with payment methods that are popular across the border, particularly for e-commerce and lifestyle spending.

4. Multi-method checkout

Hong Kong shoppers want flexibility. Merchants offering multiple payment options, such as cards, wallets and QR payments, see better conversion and higher trust, especially in online checkout flows.

The payment methods businesses must offer in Hong Kong

If you want to succeed in Hong Kong, these are the essential payment options to support:

1. Octopus

Still one of the city’s most iconic payment systems, Octopus started as a transit card (prepaid travel card) but has become a major digital wallet with millions of active users. It’s embedded into everyday life including transport, convenience stores, supermarkets, vending machines and growing e-commerce use.

Why offer it?

- Mass adoption

- Fast checkout

- Strong trust and brand recognition

- Perfect for micropayments and daily essentials

2. Credit & debit cards

Despite the rise of digital wallets, cards remain a cornerstone of payments in Hong Kong and is one of the highest card-penetration markets in Asia.

Why offer them?

- Essential for e-commerce

- Strong consumer protections

- Popular for mid-to-high-value purchases

- Highly trusted both online and offline

3. Alipay

Alipay is one of the most widely used mobile wallets in the city. It offers QR-based payments, frequent promotions, transit integrations and is a key part of the local retail experience.

Why offer it?

- Popular among younger consumers

- Easy mobile-first checkout

- Prominent in both online and offline retail

4. WeChat Pay

Thanks to Hong Kong’s close economic integration with Mainland China, WeChat Pay is widely used for shopping, dining, travel and is a must for serving both local users and Mainland tourists.

Why offer it?

- Essential for cross-border shoppers

- Strong adoption in hospitality and retail

- Integrated into Hong Kong’s digital lifestyle

5. Apple Pay, Google Pay & Samsung Pay

Mobile wallet use is growing fast, particularly for card payments made through digital wallets on smartphones and smartwatches, so it’s essential to support the biggest global digital payment methods.

Why offer them?

- Highly convenient for commuters and daily shoppers

- Contactless-first culture aligns perfectly

- Trusted ecosystem backing from major tech brands

What this means for businesses

To build trust and convert more customers in Hong Kong, businesses should aim to:

- Offer a balanced mix of cards and local wallets - This ensures you cover all major consumer segments from commuters to tourists to online shoppers.

- Keep checkout friction as low as possible - Speed matters. Hong Kong shoppers expect quick and easy “tap and go.”

- Support cross-border-friendly methods - Especially if you’re targeting consumers from Mainland China or running an e-commerce business.

- Stay open to emerging wallet features - Hong Kong’s payments ecosystem moves fast. Rewards, loyalty integrations, peer-to-peer features and transport integrations often influence user preference.

Final thoughts

Hong Kong is a dynamic, highly digital market where convenience, speed and choice shape how people pay. Whether you’re operating online, offline or both, offering the right payment mix is one of the most powerful ways to stand out, increase trust and capture more customers.

There are many moving parts that a marketplace needs to manage effectively to succeed – payouts being a huge part of that!

A study reported that 56% of sellers are willing to switch to a marketplace offering faster payouts. So if you’re treating payouts like a backend process rather than part of your strategy to have a competitive edge over the competition, you could end up losing out.

Let’s take a look at the key challenges payouts can bring a marketplace and how to overcome them.

What’s in this blog:

- Compliance: Forever changing rules

- Payout fees: Hidden and out of control

- Currency volatility & FX: Its unpredictable nature

- Settlement times: The waiting game

- Fraud: The cost of openness

- Operational complexity: Manual headaches

- Seller experience: Building or burning trust

- Finding the right payment partner

1. Compliance: Forever changing rules

Regulation is one of the biggest hurdles in any marketplace payout flow, and it only grows as you scale. KYC and KYB checks must be handled correctly to prevent fraud and meet local rules. AML screening needs to run continuously, not just at onboarding. Tax obligations differ across regions and financial authorities regularly update what they expect from platforms handling money.

The difficulty isn’t simply “ticking boxes”. It’s the never-ending nature of it. Regulations shift, territories have unique interpretations and a process that works in one country might be non-compliant in another. For many marketplaces, this becomes a maze of manual checks, duplicated effort and constant worry about whether something has been missed.

How to tackle this:

The best way to achieve this? Local experts who understand the market. They need continuous, proactive systems in place to adapt to the new rules, local laws and changing risk profiles.

By using a global payments provider, like Nomupay, who have specialists on the ground across Europe, MENA and Southeast Asia, you’ll have a team on your side helping you stay up to date with regional insights and implement the rules and systems you need to keep the regulators happy.

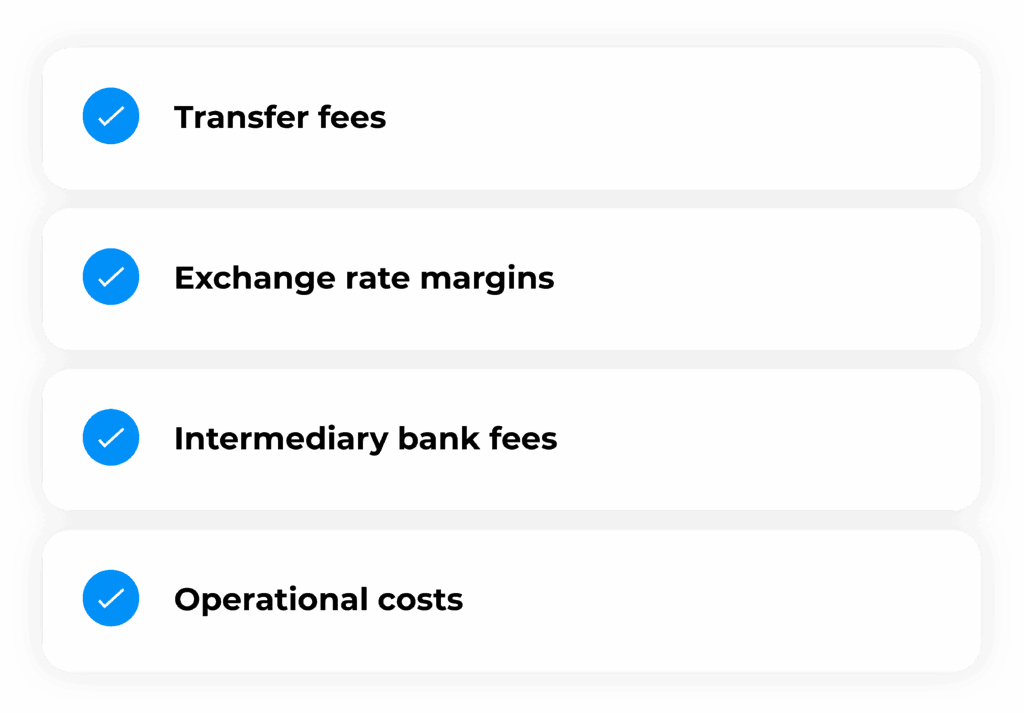

2. Payout fees: Hidden and out of control

If you’re not careful, payout fees can get out of control. Each step throughout the payout flow can incur a cost, including transfer fees, exchange rate margins, intermediary fees and operational costs. And when you’re running thousands or millions of transactions, especially when funds are being sent overseas, these costs will add up!

What makes it a challenge is the lack of transparency. Costs are often scattered across providers, banks, FX partners and internal systems. Without proper visibility, margins slowly shrink, and teams only realise when it’s already become a strategic issue.

How to tackle this:

The more players involved, the more you have to pay out, so keeping operations as simple as possible with limited systems taking a cut, will only benefit your revenue. Using a payment provider that offers the whole package, from mass payment acceptance and payouts to reporting and fraud management, you can reduce operational costs and have all your invoices in one place for complete transparency.

Sending funds in local currencies can help to tackle FX fees, as well as provide a smoother experience for the recipient.

For a full rundown of payouts and their fees, check out our blog: The hidden cost of cross-border payouts.

3. Currency volatility & FX: Its unpredictable nature

For international marketplaces, FX is a daily reality. Exchange rates move up and down constantly, and even small fluctuations can have a big impact on seller earnings. That volatility not only affects cash flow but also trust. If payees don’t understand how rates are calculated or feel shortchanged, frustration builds.

Additionally, the FX component isn’t just about rates: there are timing issues (when to convert), strategies (hedging, multi-currency balances) and communication challenges (explaining to sellers why their final payout differs from expectations). This complex mix is difficult to manage, especially at scale.

How to tackle this:

Marketplaces can ease the impact of currency volatility by offering multi-currency balances so sellers can choose when to hold or convert funds, locking in FX rates at the moment of transaction to provide certainty and a smoother experience.

Working with providers that not only have access to a range of currencies, but also offer competitive and transparent pricing to avoid unexpected costs can be invaluable in such a volatile industry.

4. Settlement times: The waiting game

Fast payouts are no longer a “nice to have”. For many sellers, they are essential. For small sellers or gig workers, delayed payouts can be crippling; cashflow can make or break their ability to operate.

Traditional banking rails, especially cross-border, simply aren’t designed for speed. Intermediaries introduce delays. Fraud checks extend timelines. Lack of flexibility creates friction. Speed isn’t just a convenience; it’s a competitive necessity.

How to tackle this:

The fastest way to settle funds is to use local payment rails, local currencies and digital wallets. By relying on a global platform with direct access to local acquirers, you simplify the process and avoid the intermediary banks that often introduce delays. Using local currencies further reduces FX-related hold-ups, and local payment methods help bypass the slow processing times of traditional banks so your funds can reach its recipient quicker and smoother.

5. Fraud: The cost of openness

Marketplaces thrive on openness. Anyone can sign up from professional sellers to one-off freelancers, start selling and get paid. Unfortunately, that also makes them ideal targets for fraudsters, including fake sellers, stolen identities, account takeovers, chargeback abuse and money laundering.

Fraud becomes especially dangerous at the payout stage. Once funds have left the platform, they’re notoriously difficult to recover. Marketplaces often rely on manual reviews or outdated tools, which can be both slow and ineffective. The constant balancing act between blocking bad actors and maintaining a smooth experience for legitimate sellers is one of the hardest operational challenges in the industry.

How to tackle this:

To tackle fraud effectively, marketplaces need a proactive approach that blends strong identity verification with real-time monitoring. Thorough KYC and KYB checks at onboarding help prevent bad actors from entering the system, while ongoing behavioural analysis and transaction monitoring can flag suspicious patterns before payouts are released.

6. Operational complexity: Manual headaches

Behind the scenes, many payout processes are held together by spreadsheets and legacy workflows. But as volume grows, complexity grows too. What worked for 500 sellers completely falls apart at 50,000.

Without strong systems in place, manual tasks like chasing missing bank details, resolving failed payments, re-issuing payouts and managing exceptions become an operational headache. These tasks not only waste time but also introduce risk with human error. As your marketplace grows, this manual complexity can become a serious bottleneck.

How to tackle this

The key to reducing operational complexity is automation and consolidation. By replacing manual reconciliation and data entry with automated workflows, marketplaces can cut errors and free up teams to focus on higher-value tasks. Using a single, unified payout platform also reduces fragmentation across systems, streamlines reporting and makes it easier to manage global payouts at scale. Together, these steps turn a previously time-consuming process into one that runs smoothly and efficiently.

7. Seller experience: Building or burning trust

For sellers, payouts are more than just another payment solution; they’re the crux of their business, meaning it’s a huge trust moment that proves whether your platform is right for them or not. A confusing fee, an unexpected delay or a failed payout can undo months of relationship-building.

Marketplaces increasingly differentiate themselves on experience, and payout experience is a major part of that. Sellers expect transparency, predictability and control. When they don’t get it, they naturally question whether your platform is the right place for them to build their business.

How to tackle this:

Clear communication, flexible payout options, multi-currency balances and transparent fee structures all contribute to a smoother, more trustworthy experience. It’s easier said than done, but if you can provide all of this, then you’re on to a winner.

With the help from a payment provider, creating this seamless experience can become a whole lot easier. That’s why choosing the right payment partner is so important.

Finding the right payment partner

One of the biggest steps in overcoming all of these challenges is finding the right payment partner who can support global marketplace payouts.

When looking for a PSP, the key things to consider include:

- Global reach with local expertise – Access to local rails, currencies and acquiring partners to reduce delays and costs.

- Strong compliance and risk management – Built-in KYC, KYB, AML and ongoing monitoring that keeps you ahead of regulatory demands.

- Transparent pricing and competitive FX – Clear fee structures and fair FX rates that protect both your margins and your sellers’.

- Fast, reliable settlement – The ability to process payouts quickly across multiple markets without relying on slow correspondent banks.

- Robust fraud prevention – Tools that detect suspicious activity early without disrupting genuine sellers.

- Operational efficiency – Automation, in-depth reporting and a unified platform that reduces manual work and operational overhead.

- Flexible payout options – Support for local payment methods, digital wallets and multi-currency balances.

Choosing the right PSP can transform payouts from a constant challenge into a competitive advantage. If you’re looking for a partner designed specifically to help marketplaces grow across borders with simplicity and confidence, Nomupay delivers the local access, flexible and speedy experience, and unified solutions needed to make global payouts seamless.

Check out our payouts page for all the details.

Cross-border payouts can take your business to the next level, but only if they’re done right. Running your payouts inefficiently can cause you to lose money rather than gain – which is less than ideal.

An important factor to understanding is the cost of sending funds internationally and all the moving parts that come with it.

So, let’s take a look at the hidden cost of cross-border payouts to avoid you getting blind-sided by fees, exchange rates and everything in between.

What’s in this blog:

- Why efficient cross-border payouts matter

- Important factors in managing cross-border payouts

- What fees do you need to be aware of

- How to keep fees to a minimum

- Choosing the right payout service

Why efficient cross-border payouts matter

Whether you’re planning to scale your business globally, or you’re already reaching an international audience, cross-border payouts are a fundamental solution that you need to get right, particularly if you’re running a marketplace.

Here are just a few reasons why you should consider payouts as a priority.

Expansion

For businesses looking to grow globally, smooth cross-border payouts are key. They make it possible to pay overseas suppliers and reach new markets without unnecessary friction. When you can pay people easily, no matter where you or the recipient is in the world, your business can expand faster and operate more flexibly.

Support a global workforce

Why restrict yourself with the team you hire! Talent is all over the world, and it’s important to have local expertise in each market you want to expand to. Being able to payout to your international workforce seamlessly is just as important as sending funds to clients.

Competitive edge

In today’s digital economy, speed and reliability matter. Companies that offer quick, transparent payouts stand out. Whether you’re an online marketplace, a gig platform or a global service provider, a seamless payout experience can build trust and loyalty among your international partners and customers.

Important factors in managing cross-border payouts

Before you take the plunge and set up cross-border payouts, you need to be aware of the logistics. Considering the following aspects should be included in your strategy.

Exchange rates

Foreign exchange (FX) rates can make a big difference to how much your business and your recipients actually receive. Even small fluctuations can add up over time. It’s important to understand how your provider sets exchange rates, and whether they use a mid-market rate (the one you see on Google) or add a margin on top.

Local regulations

Every country has its own financial rules, tax requirements and reporting standards. Staying compliant can be tricky, especially if you’re paying into multiple regions. Working with a payment partner who understands local regulations can save time, reduce risk and help you avoid unnecessary delays or penalties.

Time and costs

Cross-border transfers don’t always move as quickly as domestic ones. Traditional bank wires can take several days, and intermediary banks may charge extra along the way. Newer digital payout solutions, however, can move funds in near real-time and often at a lower cost.

What fees do you need to be aware of

When sending money internationally, there are often more players involved than you might think. Each step in the journey, from your account to the recipient’s, can add a cost, and these fees can quickly add up if you’re not careful.

Here are the main types of charges to look out for:

- Transfer fees – This is the most obvious cost. Some providers charge a flat fee per transaction, while others take a small percentage of the amount you’re sending. Even if the fee seems small, it can make a difference if you’re sending large sums or frequent payments.

- Exchange rate margins – Whenever money is converted into another currency, the exchange rate used matters. Some banks and payment providers add an additional margin rate, often hidden within the exchange rate. So it’s important to be aware of this upfront.

- Intermediary or correspondent bank fees – International payments often pass through one or more banks before reaching the recipient, and each of these banks may charge a fee.

- Operational costs – Behind the scenes, providers invest in security, compliance and processing systems. These costs are sometimes built into fees or exchange rates. Choosing a provider that balances transparency with efficiency can help minimise unnecessary charges.

Understanding where these costs come from helps you make smarter choices. By breaking down the fees and being aware of hidden charges, you can avoid unpleasant surprises and make your payouts more efficient and cost-effective.

How to keep fees to a minimum

The good news is that international payouts don’t have to be expensive. By being proactive and choosing the right tools, you can keep fees manageable and make sure more of your money reaches its destination.

Here are some practical ways to lower your costs:

- Use a specialist provider – Traditional banks often rely on older systems and multiple intermediaries, which can add layers of cost. Modern fintech providers, on the other hand, use a more efficient infrastructure, simplifying the journey – helping to keep costs low. Many also display all fees upfront, so you know exactly what you’re paying before you hit ‘send’.

- Pay in local currencies – Sending money in the recipient’s local currency can eliminate extra conversion fees at their end. It also creates a smoother experience for the people you’re paying, since they receive the exact amount they expect without exchange-rate surprises.

- Change the payment method – Bank transfers aren’t always the most cost-effective route. In many cases, sending money to digital wallets can cut out intermediary banks, shorten the payment chain and reduce fees. These methods can also speed up delivery times, which keeps your payees happier and your operations running smoothly.

- Batch your payouts – If you make frequent international transfers, for example, paying multiple freelancers or suppliers, batching them into a single transaction can help reduce processing fees. It also simplifies your accounting and may give you access to volume-based discounts from your provider.

- Be transparent and compare regularly – FX rates and fee structures can vary widely between providers, and they change over time. Make it a habit to compare exchange rates and total costs across different platforms. Even a small difference in the FX margin can add up to significant savings over months of regular payments.

Ultimately, the best way to lower fees is to stay informed and flexible. The more visibility you have over how and where your money moves, the easier it is to spot opportunities to save — and to make cross-border payouts efficient, transparent and fair for everyone involved.

Choosing the right payout service

So, we’ve talked about the benefits of using a specialist provider, but what does that actually mean in practice? The right partner can make all the difference between slow, costly transfers and fast, transparent global payouts that help your business grow.

When comparing providers, look beyond the headline fees. A great cross-border payout solution should offer:

- Transparent pricing – no hidden mark-ups or surprise deductions along the way.

- Wide reach – access to multiple countries, currencies and payment methods.

- Speed and reliability – payments that arrive quickly and consistently.

- Compliance and security – adherence to local regulations and strong fraud protection.

- Simple integration – technology that works easily with your existing systems.

We may be a little biased, but this is exactly where Nomupay fits in. Our payout solution is designed for businesses that want to move money globally without the usual complexity. With a single API and a Unified Platform, you can send payments to multiple markets, currencies and channels, all with transparency and control built in.

Nomupay takes care of the local details so you can focus on what matters most: growing your business and paying your teams, partners or customers quickly and fairly — wherever they are.

Buy Now Pay Later (BNPL) has become such an integral part of the e-commerce world. The popular payment method has continued to rise over the years, offering consumers the financial freedom they’ve now come to expect. It’s become so fundamental to the way consumers shop that 40% of shoppers will even postpone their purchase if BNPL isn’t an option.

And it’s growth doesn’t stop here. It’s predicted to

Younger shoppers are driving BNPL’s rise, preferring short-term, manageable installments over the long-term commitment of traditional credit. As much as 44% of US Gen-Z shoppers prefer its flexibility over credit cards.

From the merchant viewpoint, BNPL presents an attractive proposition, accelerate towards 900 million global users by 2027!

So, if it’s not a part of your checkout flow yet, why not? Let’s take a look at the key drivers for BNPL’s success.

What’s in this blog:

- Low risk, high reward

- Optimised checkout: Speed and simplicity

- Driving revenue

- Growing demand for flexible payments

Low risk, high reward

not just as a payment option, but as a strategic tool for acquisition, increased order value and conversion uplift.

It is often seen as less risky than extending credit themselves, because the BNPL provider typically takes on the risk themselves. You, as the merchant, will benefit from receiving the full payment upfront while offering customers flexible installments, reducing financial exposure and simplifying cash flow management.

Driving revenue

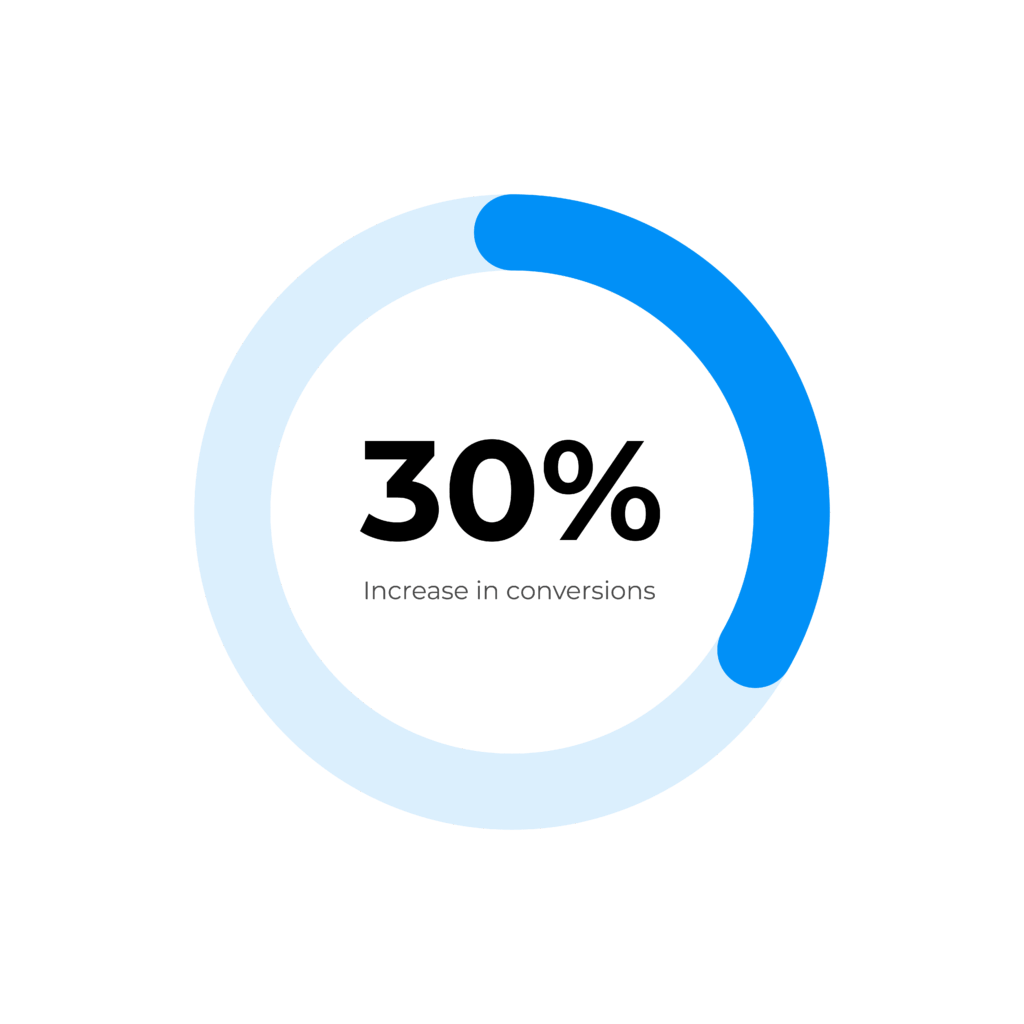

In addition to smoothing the checkout process, the availability of BNPL options in e-commerce stores have shown an increase in customer loyalty and conversions wherein sales have increased by up to 30%.

With the draw of paying for purchases over time or via installments, customers are going beyond making that first initial buying decision and are increasing their average order value by 20-40%.

In fact, in Asia-Pacific, BNPL accounts for approximately 36.4% of global provider revenue. That’s huge for a single payment method!

Optimised checkout: Speed and simplicity

With multiple BNPL options available to consumers through the likes of Klarna, Clear Pay, Affirm and PayPal's pay in 3 (UK) option, these payment methods are increasingly becoming the standard at checkout.

It enforces convenience, which is now an expectation, alongside auto-fill and real-time validation, with 76% of consumers saying a smooth checkout is very influential when choosing a merchant.

BNPL acts as a one-click checkout option for shoppers that either don't have the immediacy of funds or aren't willing to submit payment information across numerous sites. Ultimately, BNPL sits as a contender alongside of, and works with, e-wallet fast payment options, to provide a convenient and speedy way of checking out.

Growing demand for flexible payments

The demand for alternative payment methods is there, with BNPL being just one sector of this massively increasing market. In the UK alone, 61% of consumers say they are more likely to shop with a retailer offering BNPL. That’s a huge market you could be missing out on if you decide against offering it.