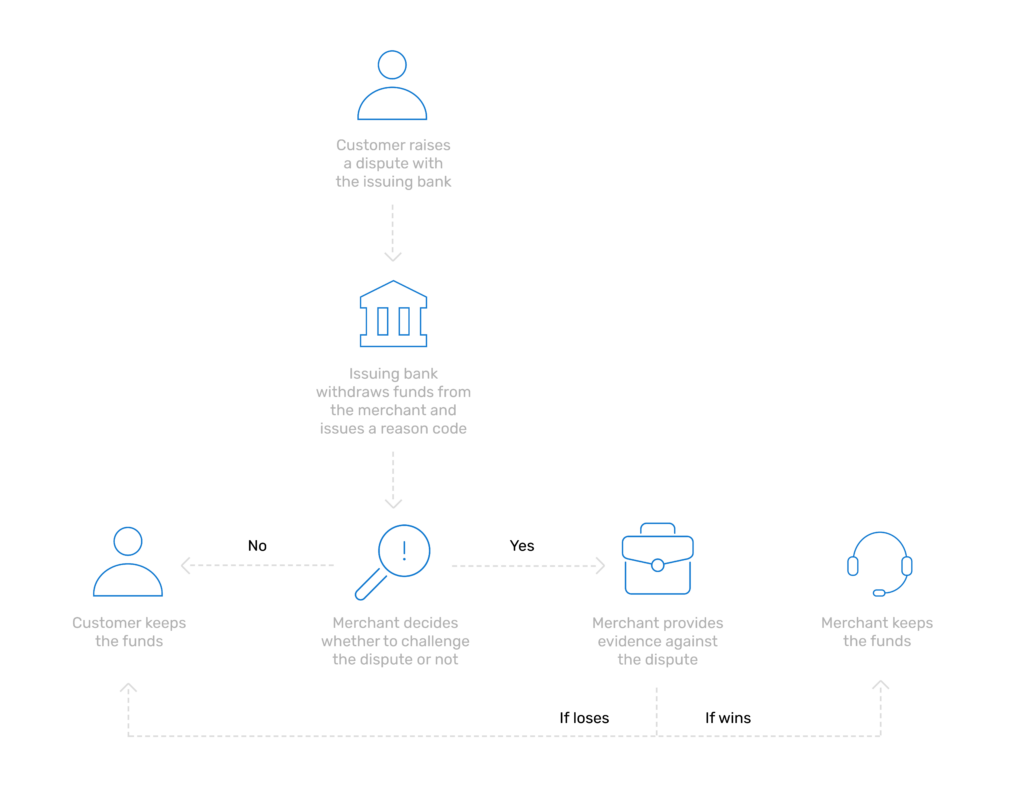

A chargeback occurs when a cardholder contacts their card issuing bank and claims that a particular transaction on their bank statement is not valid. The aim of the cardholder is to receive their money back. There are several reasons why a cardholder may file a dispute, and they are discussed in a separate article, so check it out as well.

This article focuses on the chargeback process and the possible outcomes, so let’s look at it in detail.

A cardholder disputes a transaction.

The card issuing bank receives the dispute information and decides whether the dispute is valid or invalid.

If the issuing bank decides that the dispute is not valid, the chargeback process ends.

If the dispute appears to be valid, the issuing bank credits the disputed transaction amount to the cardholder and informs the merchant's acquiring bank of the dispute.

The acquiring bank receives the information about the chargeback and informs the merchant about it.

The merchant has the right to prove that the transaction was valid. However, they can also ignore the chargeback and automatically lose the disputed funds.

If the merchant decides to prove the validity of the transaction, they must gather and provide compelling evidence. The evidence may include the whole communication with the customer, tracking numbers, delivery receipts and other documents.

Chargeback resolution

The merchant sends the evidence to their acquiring bank.

The acquiring bank then transmits it further to the cardholder’s issuing bank.

The decision who wins the chargeback is entirely in the hands of the issuing bank. Therefore, it is vital for the merchant to collect and present all the data that will confirm the legitimacy of the transaction.

If the issuing bank comes to the conclusion that the evidence provided by the merchant is sufficient, the merchant wins the chargeback and retains the money.

If the issuing bank decides that the merchant’s evidence is inadequate, the cardholder wins the chargeback and the funds remain with them.

Pre-arbitration and arbitration

If the cardholder has lost the chargeback but is still certain that the transaction was invalid, they have the right to dispute it again. This is referred to as pre-arbitration or a second chargeback. The whole chargeback cycle repeats.

If the merchant wins pre-arbitration, but the cardholder is determined to prove that his dispute is valid, the issuing bank can call for arbitration. The arbitration process is highly expensive for the merchant if the cardholder wins.

Every step in the chargeback process has its set time frames. Even though the merchant should act as quickly as possible, the investigation may take a longer period of time. It should also be noted that a merchant may receive a chargeback even if the transaction was made several months ago. So, be always prepared to take risks and learn how to prevent chargebacks from happening.

Make sure to keep in touch with your payment service provider during the chargeback process and provide all the essential information about the disputed order.